By Marvin Gandis

One of the reasons many people make poor financial decisions is desperation.

- They want quick results.

- They want immediate money.

- They want to get out of debt overnight.

- They want to build wealth without a process.

- They want to change their lives without waiting, planting, or developing discipline.

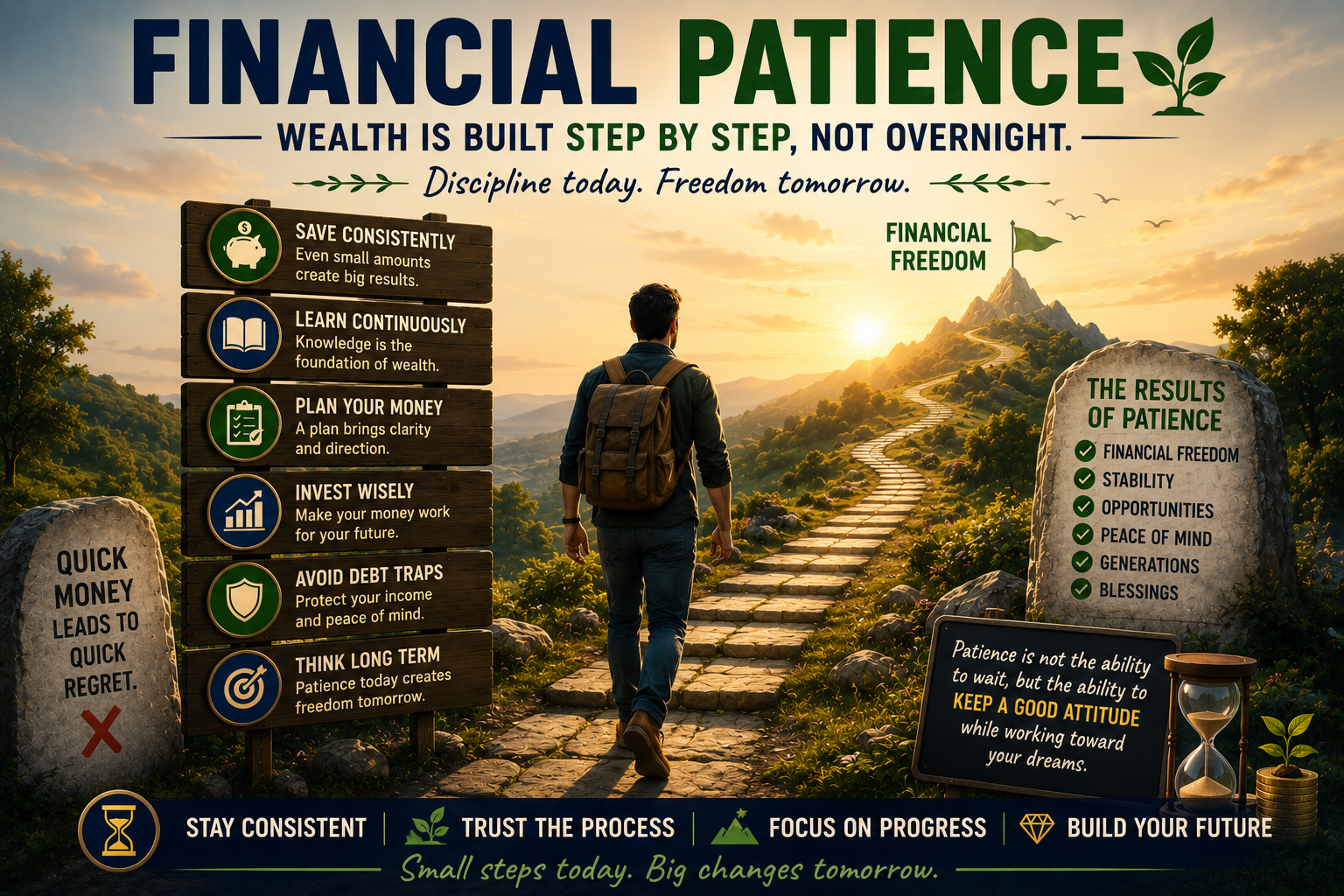

But solid wealth rarely comes from desperation. It comes from patience, education, order, consistency, and decisions repeated with wisdom.

In this eleventh part of the series “The Reverse Question,” we will reflect on the importance of financial patience.

- Not as an excuse to remain inactive.

- Not as conformity.

- Not as passivity.

But as a way to build with vision, without allowing anxiety to control our decisions.

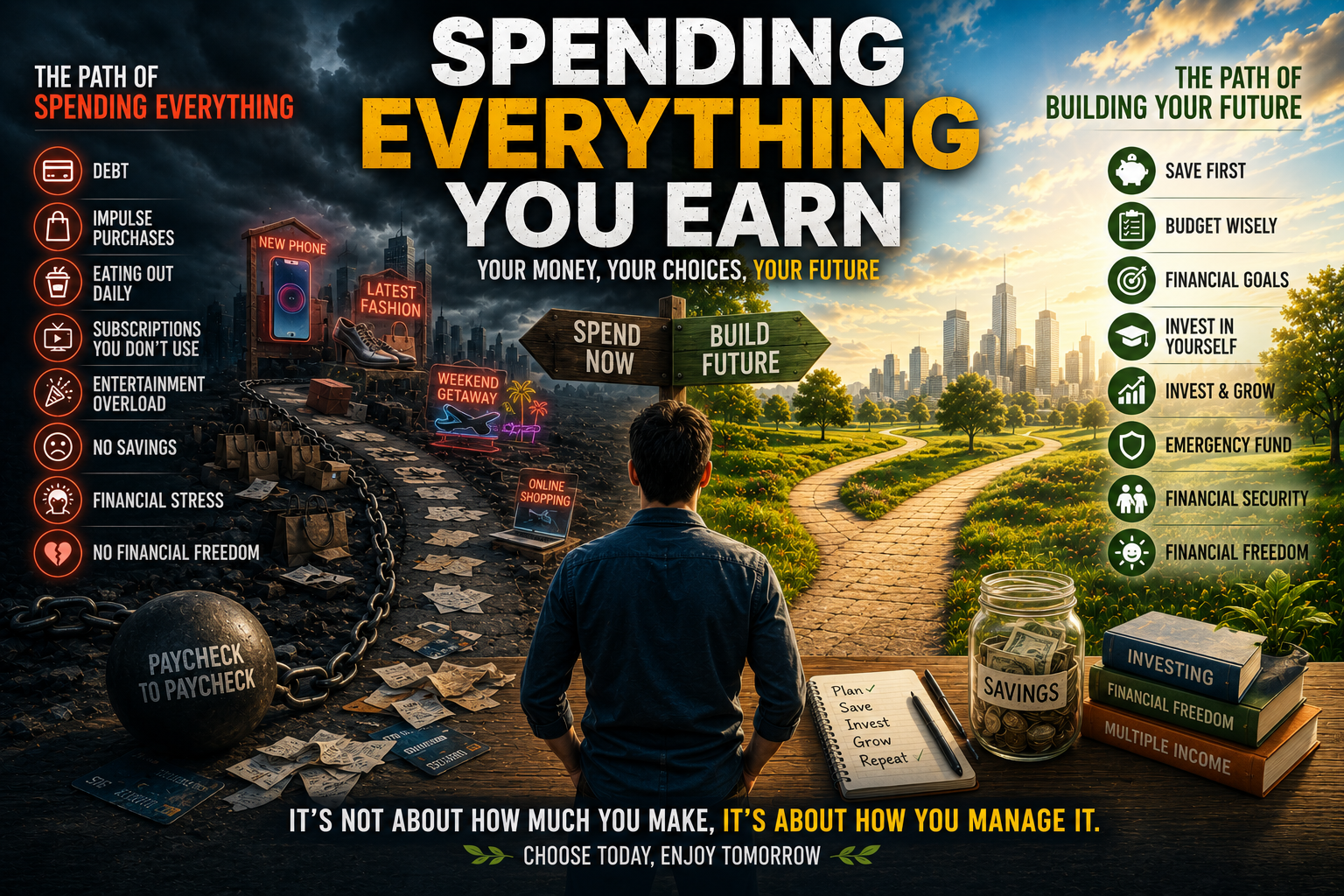

Desperation can be expensive

When a person is desperate, they can make decisions that seem good in the moment but create more pain later.

- They can fall into unnecessary debt.

- They can invest in false promises.

- They can buy programs without understanding them.

- They can abandon a correct process too soon.

- They can constantly switch opportunities.

- They can spend out of anxiety.

- They can sell under pressure.

- They can accept agreements that are not good for them.

Desperation reduces clarity.

When a person feels they must solve everything immediately, they may lose the ability to analyze, compare, ask questions, wait, and decide with wisdom.

That is why financial patience is not a weakness. It is protection.

Solid wealth needs time

Many people want a harvest without a season of planting.

But life works by principles.

- First, you learn.

- First, you organize.

- First, you plant.

- First, you practice.

- First, you correct.

- First, you remain consistent.

Then, with time, fruit may appear.

True wealth is not built only through one big opportunity. It is built through small repeated habits: saving, learning, investing carefully, reducing debt, creating value, working consistently, and improving money management.

Small actions, repeated with discipline, can become large over time.

Patience does not mean standing still

Some people confuse patience with doing nothing.

But financial patience is not sitting around waiting for life to change. It is acting consistently while results mature.

- Patience is saving, even if it is a little.

- Patience is learning, even if you do not see income yet.

- Patience is paying off debt little by little.

- Patience is building a business without quitting at the first obstacle.

- Patience is improving a skill before demanding major results.

- Patience is reviewing your numbers even when they are uncomfortable.

- Patience is saying “no” to expenses that destroy your future.

- True patience is active.

- It does not quit.

- It does not rush without thinking.

- It does not abandon the process because of anxiety.

The long-term mindset

A person with a long-term mindset understands that not every decision must produce an immediate reward.

- Sometimes saving today protects tomorrow.

- Sometimes studying today opens doors later.

- Sometimes investing in a skill today produces income years later.

- Sometimes rejecting an expense today avoids future debt.

- Sometimes planting content today builds trust over time.

The short-term mindset asks:

“What can I get now?”

The long-term mindset asks:

“What am I building for tomorrow?”

That difference changes the way a person spends, works, learns, invests, and decides.

The danger of quick money

The desire for quick money can lead to many traps.

Not every opportunity is bad. Not every business is false. Not every tool is useless. But when a person looks for quick money without education, analysis, and patience, they become vulnerable.

- They may believe any promise.

- They may trust anyone.

- They may invest without research.

- They may go into debt because of emotion.

- They may chase magical formulas.

- They may ignore warning signs.

Quick money often attracts quick decisions. And quick decisions, without wisdom, can be expensive.

Before entering an opportunity, a person should ask:

- Do I understand how this works?

- Am I making this decision out of anxiety?

- Can I handle the risk?

- Have I researched enough?

- Does this build something real or only promise excitement?

- Am I looking for a solution or escaping my frustration?

Patience protects your habits

When a person is impatient, they abandon healthy habits because they do not see immediate results.

- They stop saving because the savings seem small.

- They stop learning because they do not see quick income.

- They stop posting because nobody responds at first.

- They stop investing in themselves because visible changes are slow.

- They stop budgeting because debts still exist.

- They stop building because the process feels slow.

But many valuable things begin small.

- A small saving can become an emergency fund.

- A small lesson can become a skill.

- A small improvement can become confidence.

- A small daily action can become a transformation.

Patience protects what is small until it grows.

Discipline defeats anxiety

Financial anxiety can cause a person to live in reaction mode.

- They react to bills.

- They react to debt.

- They react to emergencies.

- They react to pressure.

- They react to fear.

- They react to what others say.

Discipline helps recover direction.

- A budget reduces confusion.

- A debt plan reduces fear.

- An emergency fund reduces vulnerability.

- A learning routine increases ability.

- A follow-up system improves results.

- A daily action plan reduces improvisation.

Discipline does not eliminate every problem, but it reduces disorder.

And where there is less disorder, there is more peace to make decisions.

Building wealth without comparing yourself

Comparison destroys patience.

- You see someone buying a house, and you feel left behind.

- You see someone showing a business, and you feel like a failure.

- You see someone traveling, and you feel your life is not moving.

- You see someone appearing successful, and you pressure yourself to run.

But you do not always know the full story behind others.

- You do not know their debts.

- You do not know their sacrifices.

- You do not know their years of process.

- You do not know their mistakes.

- You do not know their family reality.

- You do not know what is behind the image.

Comparing yourself with others can lead you to make decisions to impress, not to build.

Your process needs patience, not constant competition.

Practical steps to develop financial patience

1. Define realistic goals

Do not only say: “I want to be rich.”

Define clear goals:

- Save a specific amount.

- Reduce a debt.

- Create an emergency fund.

- Learn a skill.

- Increase income gradually.

- Organize expenses.

- Invest in education.

- Build a long-term project.

Clear goals help reduce anxiety.

2. Divide the process into stages

Not everything has to be solved today.

- First organize.

- Then reduce unnecessary expenses.

- Then create a margin.

- Then save.

- Then pay debt strategically.

- Then learn more.

- Then invest carefully.

- Then build new sources of value.

Patience grows when you understand that the path has stages.

3. Celebrate small progress

Do not wait until the end to recognize advancement.

- If you saved something, you moved forward.

- If you paid a debt, you moved forward.

- If you learned a skill, you moved forward.

- If you avoided an impulsive purchase, you moved forward.

- If you reviewed your numbers, you moved forward.

- If you made a wise decision, you moved forward.

Small progress also deserves respect.

4. Learn before investing

Never allow pressure to lead you into investing in something you do not understand.

Before putting in money, invest time in learning.

- Research.

- Ask questions.

- Compare.

- Read.

- Consult.

- Analyze risks.

- Review whether the opportunity is realistic.

- Do not confuse emotion with evidence.

Patience before investing can prevent pain later.

5. Build habits, not only desires

Wanting wealth is not enough.

You need habits.

- A habit of saving.

- A habit of learning.

- A habit of measuring.

- A habit of reducing debt.

- A habit of creating value.

- A habit of following up.

- A habit of reviewing results.

- A habit of correcting.

- A habit of continuing.

Desires inspire, but habits build.

Financial patience can also require faith

For many people, building with patience also requires faith.

- Faith to keep planting when fruit is not visible yet.

- Faith to correct without quitting.

- Faith to learn even when it is uncomfortable.

- Faith to manage a little with wisdom before receiving more.

- Faith to believe that a life can change step by step.

Faith does not remove responsibility. It strengthens it.

Because mature faith does not only wait. It also works, learns, serves, manages, and perseveres.

Conclusion

Financial patience is not passivity. It is discipline with vision.

It is the ability to build without desperation, decide without anxiety, learn before acting, save before spending, correct before quitting, and think about the future before sacrificing it for an emotion in the present.

My dear reader or friend, do not allow desperation to steal your wisdom. Not everything has to be solved today. Not every fruit appears quickly. Not every seed shows results immediately.

But if you continue learning, managing, correcting, creating value, and walking with consistency, you can begin to build a more stable life.

Solid wealth is not improvised.

- It is planned.

- It is learned.

- It is managed.

- It is planted.

- It is protected.

- It is built.

And many times, it is built slowly, until one day the results begin to show that patience was not wasted time, but preparation.

Disclaimer

This article is for educational, reflective, and informational purposes only. It should not be interpreted as financial, legal, accounting, professional, business, or investment advice. The purpose of this content is to encourage awareness about financial patience, discipline, saving, planning, financial education, and responsible decision-making.

Every person has a different financial reality. Income, expenses, debt, family responsibilities, opportunities, risks, resources, and results can vary widely. Financial patience may help support better decisions, but it does not guarantee wealth, income, business success, profitable investments, or specific results.

Before making important decisions related to money, debt, investments, business, budgeting, career, or personal finances, it is recommended to consult qualified professionals.

The information shared is intended to inspire reflection, preparation, and responsible action.

Debe estar conectado para enviar un comentario.