Lo que nadie ve determina lo que algún día todos podrán ver

Por Marvin Gandis

Vivimos en una época obsesionada con los resultados.

Queremos crecimiento rápido, ingresos rápidos, reconocimiento rápido, negocios exitosos, relaciones saludables, estabilidad financiera, paz emocional y respuestas inmediatas.

Queremos los frutos.

Pero pocas veces hablamos de las raíces.

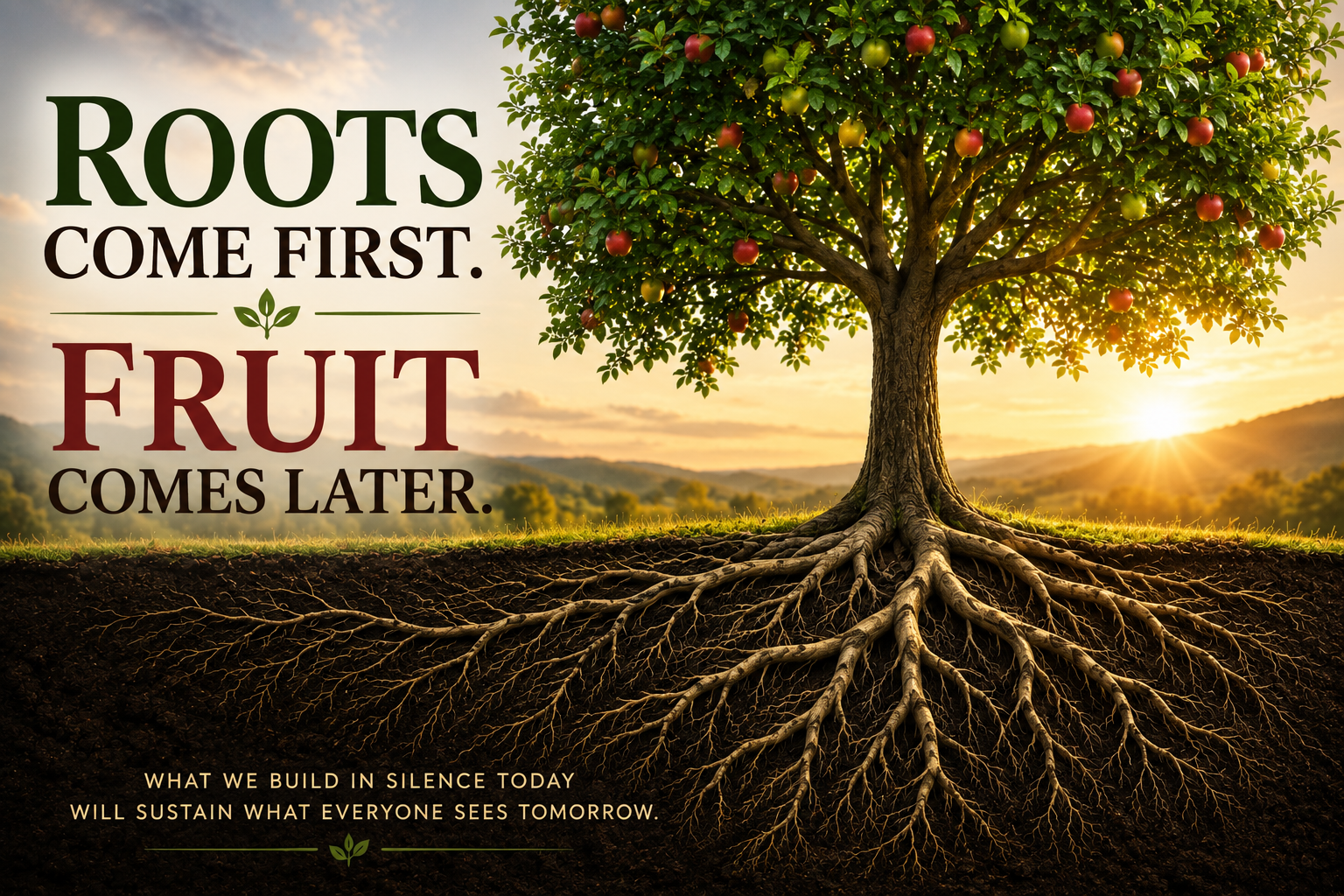

Un árbol no comienza produciendo frutos. Primero desarrolla raíces. Se afirma en la tierra. Busca agua. Absorbe nutrientes. Resiste temporadas difíciles. Crece silenciosamente donde nadie puede verlo.

Solo después aparece aquello que todos admiran.

La vida funciona de manera muy parecida.

Las raíces vienen primero. Los frutos vienen después.

Esta sencilla verdad puede cambiar nuestra manera de entender el éxito, la fe, el dinero, las relaciones, el trabajo y nuestro propio desarrollo.

El mundo celebra los frutos, pero rara vez observa las raíces

Cuando vemos a una persona exitosa, normalmente vemos el resultado.

Vemos el negocio.

La casa.

El conocimiento.

La confianza.

La audiencia.

El ministerio.

La estabilidad.

Los logros.

Pero no vemos fácilmente los años de preparación, los errores, las noches difíciles, las decisiones incómodas, las oportunidades rechazadas, las habilidades desarrolladas, las oraciones silenciosas y las veces que esa persona tuvo que comenzar nuevamente.

Estamos observando los frutos sin haber presenciado las raíces.

Ese es uno de los grandes peligros de compararnos con otras personas.

Comparamos nuestro proceso invisible con los resultados visibles de alguien más.

Y entonces pensamos que estamos atrasados.

Tal vez no lo estamos.

Quizás simplemente estamos en una temporada de raíces.

El crecimiento más importante muchas veces ocurre donde nadie puede verlo

Cuando una semilla es colocada bajo tierra, aparentemente desaparece.

Durante un tiempo no hay árbol.

No hay flores.

No hay frutos.

Desde la superficie parece que nada está sucediendo.

Sin embargo, debajo de la tierra ha comenzado una transformación extraordinaria.

La semilla está cambiando.

Las raíces están apareciendo.

La vida se está preparando.

Lo mismo puede suceder con nosotros.

Hay temporadas en las que estudiamos y nadie lo nota.

Trabajamos y nadie aplaude.

Ahorramos y nadie lo celebra.

Oramos y todavía no vemos respuesta.

Publicamos contenido y casi nadie responde.

Construimos un proyecto y los resultados parecen insignificantes.

Aprendemos nuevas habilidades mientras otros parecen avanzar mucho más rápido.

No confundamos falta de visibilidad con falta de progreso.

Algunas de las etapas más importantes de nuestra vida ocurren bajo la superficie.

Las raíces representan aquello que sostiene nuestra vida

Nuestras raíces no son visibles, pero determinan nuestra capacidad para permanecer firmes.

Entre esas raíces podemos encontrar:

- carácter,

- disciplina,

- conocimiento,

- fe,

- principios,

- hábitos,

- paciencia,

- integridad,

- educación,

- experiencia,

- relaciones saludables,

- capacidad de administrar recursos,

- perseverancia.

Los frutos representan los resultados que nacen de esas raíces:

oportunidades, influencia, estabilidad, prosperidad, liderazgo, confianza, relaciones sólidas y resultados duraderos.

El error aparece cuando intentamos conseguir los frutos sin desarrollar aquello que debe sostenerlos.

Frutos sin raíces pueden convertirse en una bendición demasiado pesada

No todo crecimiento rápido es crecimiento saludable.

Imaginemos recibir hoy diez veces más dinero sin haber aprendido a administrarlo.

O conseguir miles de clientes sin tener sistemas para atenderlos.

O recibir una posición de liderazgo sin haber desarrollado carácter.

O alcanzar una enorme audiencia sin tener claridad sobre nuestro mensaje.

Aquello que parecía una bendición puede convertirse rápidamente en una carga.

Por eso algunas veces la preparación debe preceder a la oportunidad.

No porque no merezcamos avanzar, sino porque la capacidad debe crecer junto con la oportunidad.

Antes de pedir frutos mayores, quizá debamos preguntarnos:

¿Mis raíces pueden sostenerlos?

Raíces financieras antes que prosperidad financiera

Esta enseñanza es especialmente importante cuando hablamos de dinero.

Muchas personas quieren más ingresos.

Eso es comprensible.

Pero aumentar los ingresos sin mejorar nuestros hábitos financieros no necesariamente produce estabilidad.

Las raíces financieras incluyen:

presupuesto, ahorro, reducción responsable de deudas, educación financiera, inversión prudente, creación de habilidades, diversificación razonable de ingresos y disciplina para diferenciar deseos de necesidades.

El dinero amplifica comportamientos.

Si una persona administra mal $1,000, ganar $10,000 no garantiza automáticamente que aprenda a administrarlos.

Por eso la verdadera prosperidad comienza antes del dinero.

Comienza con conocimiento y comportamiento.

Primero, administración. Después expansión.

Raíces antes que resultados en los negocios

Internet puede hacernos creer que construir un negocio es extremadamente rápido.

Vemos anuncios prometiendo resultados extraordinarios.

Pero detrás de cualquier negocio sostenible normalmente existen fundamentos menos emocionantes:

Comprender al cliente, aprender a comunicar valor, desarrollar una oferta útil, generar confianza, construir una audiencia, aprender marketing, crear sistemas, medir resultados y mejorar constantemente.

Estas actividades pueden parecer pequeñas.

Pero son raíces.

Una campaña publicitaria puede producir ventas.

Una audiencia que confía en nosotros puede producir ventas durante años.

Existe una enorme diferencia.

Raíces antes que influencia

Hoy cualquier persona puede publicar contenido.

Pero publicar no significa necesariamente influir.

La verdadera influencia se construye mediante confianza.

Y la confianza normalmente necesita tiempo.

Cada artículo útil es una raíz.

Cada correo que realmente ayuda al lector es una raíz.

Cada respuesta respetuosa es una raíz.

Cada promesa cumplida es una raíz.

Cada ocasión en que decidimos enseñar en lugar de presionar es una raíz.

Con el tiempo, esas pequeñas acciones pueden convertirse en reputación.

Y la reputación puede convertirse en influencia.

Raíces espirituales antes de las pruebas

Jesús utilizó repetidamente imágenes relacionadas con semillas, árboles, viñas y frutos para enseñar verdades espirituales.

En la parábola del sembrador, incluso habló de semillas que crecieron rápidamente pero no pudieron permanecer porque “no tenían raíz” (Mateo 13:5–6, 20–21).

La apariencia inicial de crecimiento no fue suficiente.

Necesitaban profundidad.

La misma enseñanza sigue siendo relevante.

La fe no debe desarrollarse solamente cuando llega la tormenta.

La oración, el conocimiento de la Palabra, la comunión con Dios, la obediencia, la gratitud y el servicio son raíces espirituales que se desarrollan diariamente.

Cuando llegan temporadas difíciles, descubrimos cuánto hemos profundizado.

Jeremías 17:7–8 describe a quien confía en el Señor como un árbol plantado junto a las aguas, que extiende sus raíces hacia la corriente y continúa dando fruto aun en tiempos difíciles.

La fortaleza visible comienza con una raíz invisible.

Dios frecuentemente trabaja primero debajo de la superficie

José recibió sueños antes de recibir autoridad.

David fue ungido antes de ocupar el trono.

Moisés pasó años en el desierto antes de dirigir al pueblo de Israel.

Los discípulos caminaron con Jesús y aprendieron antes de llevar el Evangelio a otras naciones.

Entre el llamado y el cumplimiento hubo preparación.

Entre la semilla y el fruto hubo raíces.

Por eso una temporada de espera no necesariamente significa abandono.

Puede ser una temporada de formación.

Tal vez algunas cosas que todavía no podemos ver están desarrollando precisamente la capacidad que necesitaremos mañana.

No desentierres constantemente la semilla para comprobar si está creciendo

Existe una imagen sencilla que explica uno de nuestros errores más comunes.

Imaginemos plantar una semilla hoy.

Mañana la desenterramos para comprobar si está creciendo.

La volvemos a plantar.

Dos días después hacemos lo mismo.

Nunca le damos suficiente tiempo para establecerse.

En la vida hacemos algo parecido.

Comenzamos un proyecto.

A las dos semanas cambiamos.

Probamos otra estrategia.

La abandonamos.

Compramos otro curso.

Comenzamos otro negocio.

Cambiamos nuevamente.

Siempre estamos sembrando.

Nunca permanecemos suficiente tiempo para desarrollar raíces.

La paciencia no significa permanecer indefinidamente en algo que claramente no funciona.

Debemos medir, aprender y corregir.

Pero existe una diferencia entre adaptarse inteligentemente y abandonar constantemente.

Las tormentas revelan la profundidad de las raíces

Un árbol fuerte no demuestra toda su fortaleza durante un día tranquilo.

La tormenta la revela.

Lo mismo sucede con nosotros.

Las dificultades revelan nuestras raíces.

Cuando perdemos una oportunidad.

Cuando un proyecto fracasa.

Cuando alguien nos rechaza.

Cuando nuestros ingresos disminuyen.

Cuando nuestros planes cambian.

¿Cuándo debemos comenzar nuevamente?

En esos momentos descubrimos qué hemos construido dentro de nosotros.

El éxito puede mostrar nuestros frutos.

La adversidad revela nuestras raíces.

No todas las raíces producen buenos frutos

También debemos examinar qué estamos cultivando.

Una raíz de resentimiento puede producir amargura.

Una raíz de miedo puede producir inmovilidad.

Una raíz de orgullo puede impedirnos aprender.

Una raíz de comparación puede robarnos satisfacción.

Una raíz de irresponsabilidad puede producir problemas financieros.

Por eso no basta con tener raíces.

Necesitamos raíces saludables.

Debemos preguntarnos periódicamente:

¿Qué pensamientos estoy alimentando?

¿Qué hábitos estoy fortaleciendo?

¿Qué personas están influyendo sobre mí?

¿Qué estoy aprendiendo?

¿Qué estoy practicando repetidamente?

¿En qué estoy colocando mi confianza?

Porque aquello que alimentamos debajo de la superficie eventualmente aparecerá encima de ella.

La cosecha necesita tiempo

Existe una verdad que nuestra cultura de gratificación inmediata no disfruta escuchar:

Algunas cosas importantes simplemente necesitan tiempo.

No podemos acelerar artificialmente cada proceso.

Una reputación necesita tiempo.

Una relación necesita tiempo.

La experiencia necesita tiempo.

La confianza necesita tiempo.

La sabiduría necesita tiempo.

Un negocio sostenible normalmente necesita tiempo.

La madurez espiritual necesita tiempo.

Podemos trabajar inteligentemente.

Podemos aprender más rápido.

Podemos utilizar mejores herramientas.

Podemos evitar errores innecesarios.

Pero todavía existe una ley fundamental:

Sembrar, cultivar, esperar y cosechar.

¿Qué hacer cuando todavía no aparecen los frutos?

Cuando los resultados tardan, no debemos limitarnos a esperar pasivamente.

Podemos trabajar en nuestras raíces.

Aprender una habilidad nueva.

Leer.

Estudiar.

Mejorar nuestro mensaje.

Organizar nuestras finanzas.

Fortalecer nuestra salud y nuestras relaciones.

Corregir malos hábitos.

Construir sistemas.

Servir mejor.

Escuchar más.

Orar.

Examinar nuestros resultados.

Eliminar aquello que no funciona.

Continuar sembrando aquello que sí demuestra valor.

Una temporada sin frutos visibles puede convertirse en una extraordinaria temporada de preparación.

La pregunta que cambia nuestra perspectiva

En lugar de preguntar solamente:

“¿Por qué todavía no tengo resultados?”

Podemos comenzar a preguntar:

“¿Qué raíces necesito desarrollar para sostener los resultados que deseo?”

Esa pregunta cambia todo.

Si queremos mejores finanzas, necesitamos mejores raíces financieras.

Si queremos mejores relaciones, necesitamos raíces de comunicación, respeto y paciencia.

Si queremos un negocio más grande, necesitamos mejores sistemas.

Si queremos influencia, necesitamos credibilidad.

Si queremos liderazgo, necesitamos carácter.

Si queremos permanecer firmes durante las dificultades, necesitamos profundidad espiritual.

El fruto nos dice lo que deseamos alcanzar.

Las raíces nos dicen en quién necesitamos convertirnos.

Las raíces vienen primero

Mi Estimado Lector o Amigo:

Tal vez estás trabajando y todavía nadie lo reconoce.

Tal vez estás aprendiendo y todavía no puedes demostrar grandes resultados.

Tal vez estás sembrando mientras otros parecen estar cosechando.

No midas toda tu vida solamente por aquello que puedes mostrar hoy.

Examina también aquello que estás construyendo dentro de ti.

Porque un día las raíces que nadie vio pueden sostener los frutos que muchos sí podrán ver.

No persigas solamente los frutos.

Construye raíces capaces de sostenerlos.

Profundiza antes de expandirte.

Aprende antes de enseñar.

Administra antes de multiplicar.

Sirve antes de buscar reconocimiento.

Desarrolla carácter antes de buscar influencia.

Fortalece tu fe antes de que llegue la tormenta.

Y recuerda:

La semilla no se avergüenza porque todavía no parece un árbol.

Está haciendo exactamente lo que necesita hacer.

Está echando raíces.

Y cuando las raíces son profundas, saludables y fuertes, los frutos tienen dónde permanecer.

Las raíces vienen primero.

Los frutos vienen después.

Reflexión final

No preguntes solamente:

¿Dónde están mis frutos?

Pregúntate también:

¿Cómo están mis raíces?

Porque muchas veces el futuro que deseamos no comienza con aquello que recibimos.

Comienza con aquello en lo que nos estamos convirtiendo.

Descargo de Responsabilidad

Este artículo tiene fines educativos, informativos, motivacionales y de reflexión. Las referencias relacionadas con crecimiento personal, negocios, finanzas, éxito y prosperidad no constituyen asesoramiento financiero, profesional, legal ni de inversión, ni garantizan resultados específicos. Los resultados individuales pueden variar según las circunstancias, decisiones, preparación, esfuerzo y otros factores. Las referencias bíblicas y espirituales se presentan con propósitos de reflexión y formación cristiana. Se recomienda evaluar responsablemente cualquier decisión financiera, empresarial o personal y, cuando corresponda, consultar con profesionales cualificados.

Debe estar conectado para enviar un comentario.