By Marvin Gandis

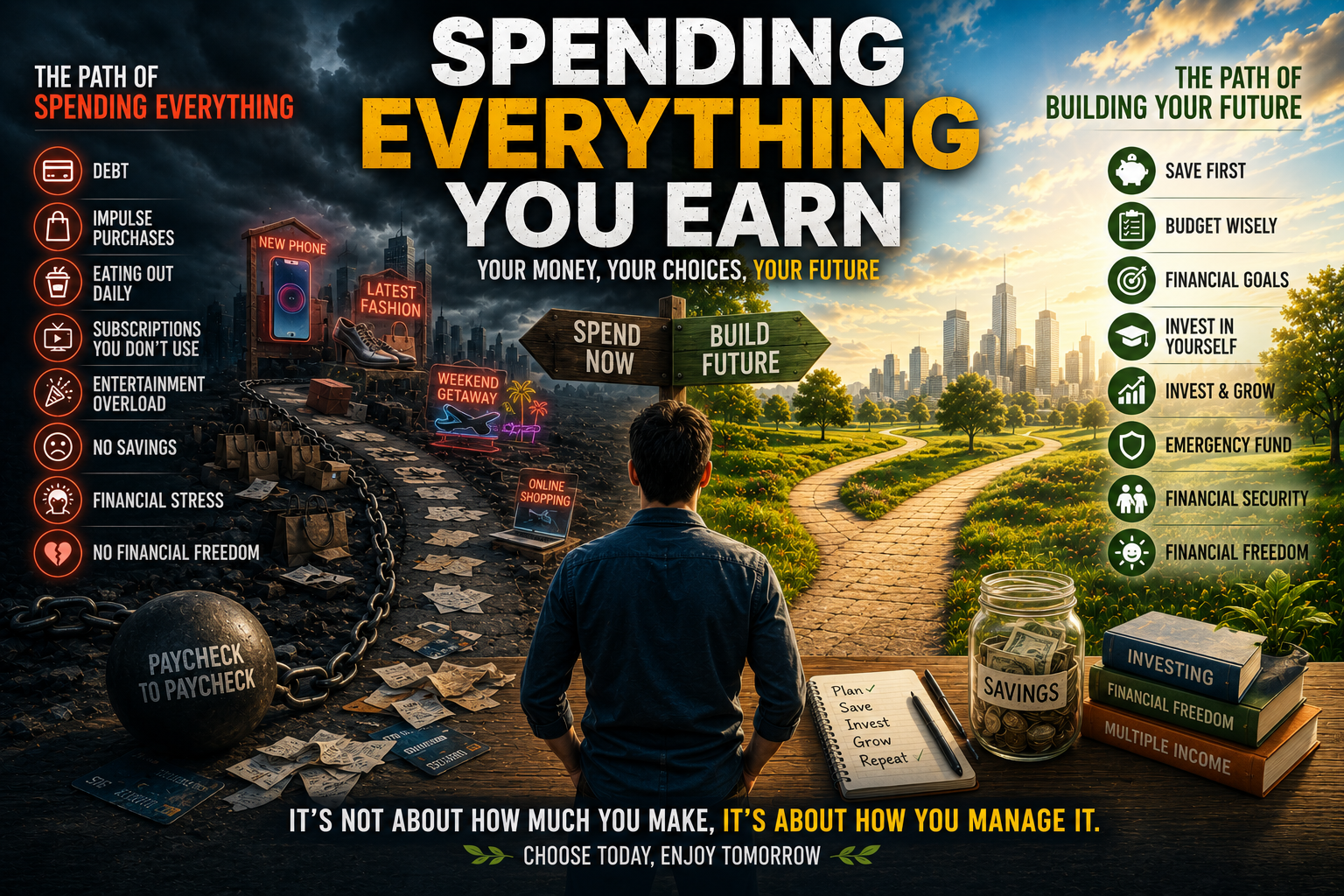

One of the most common ways to remain financially stuck is not always earning too little. Many times, you are spending everything you earn.

Some people receive little money and spend it all. But some people earn a good income and still live under pressure, in debt, worried, and without stability. This teaches us an important truth: the problem is not always only how much money comes in, but how that money is managed.

Earning more can help, but if a person does not change their financial habits, more money can simply become more expenses, more debt, more commitments, and more pressure.

In this third part of the series “The Reverse Question,” we will reflect on the silent habit of spending everything you earn, why it destroys the future, and how to begin building a more organized, wise, and responsible financial life.

- This is not about being afraid of money.

- This is not about never enjoying life.

- This is not about condemning anyone who is going through financial difficulty.

It is about learning to use money with direction, purpose, and awareness.

Money without organization disappears

Money without direction disappears quickly.

It can disappear through small purchases, impulsive spending, unnecessary payments, forgotten subscriptions, debt interest, eating out, entertainment, cravings, unplanned emergencies, or commitments that are never reviewed.

Many times, a person says:

“I don’t know where the money went.”

That phrase reveals a reality: when money does not have a plan, anything can take it away.

Money needs an assignment. It needs purpose. It needs order. If money is not given direction, it becomes smoke: it comes in, moves around, and disappears.

Spending everything creates vulnerability

When a person spends everything they earn, they live without margin.

And living without margin means living exposed.

- An unexpected expense becomes a crisis.

- A car repair becomes debt.

- A medical emergency becomes anxiety.

- A week with a lower income becomes desperation.

- An opportunity appears, but cannot be taken because there are no resources.

Lack of financial margin not only affects the wallet. It also affects the mind, peace, family, decisions, and confidence.

A person without margin often does not make decisions from wisdom, but from urgency.

The danger of living only for the present

Enjoying the present is not wrong. Life should also be appreciated and lived. The problem appears when a person lives only for the present and never thinks about tomorrow.

- They spend today without thinking about tomorrow.

- They buy today without measuring consequences.

- They go into debt today to impress others.

- They consume today to escape stress.

- They ignore the future because it feels far away.

But the future always arrives.

And when it arrives, it brings questions:

- What did you do with what you received?

- What did you build with your time?

- What did you prepare for an emergency?

- What did you learn?

- What did you save?

- What did you plant?

Living only for the present may feel good for a moment, but it can create pain tomorrow.

Spending to impress

One of the most dangerous habits is spending money to look like we are doing better than we really are.

Social media has increased this pressure. Many people feel they must show success, luxury, travel, clothes, restaurants, appearances, and achievements, even if inside they are in debt or emotionally exhausted.

But looking wealthy is not the same as building wealth.

A healthy financial life does not need to impress everyone. It needs to be sustained with order, discipline, and truth.

- Buying to be seen can become a prison.

- Spending to impress can destroy peace.

- Living for appearances can prevent building real foundations.

True prosperity does not always make noise. Sometimes it grows quietly, through small, wise, consistent decisions.

When earning more does not solve the problem

Many people believe everything would be solved if they earned more money. And it is true that higher income can relieve many burdens. But if the habit of spending everything does not change, the problem may continue.

- Some people earn little and are in debt.

- There are people who earn a lot and are also in debt.

- There are people who increase their income and increase their expenses at the same time.

- Some people receive extra money and spend it before organizing it.

This can be called living up to your income, or even beyond your income.

If every increase in income automatically becomes an increase in spending, the person never moves forward. They only change the size of their pressure.

The solution is not only to earn more. The solution is also to manage better.

The first step: know where your money goes

You cannot correct what you do not measure.

A person needs to look at their numbers honestly. Not to feel guilty, but to wake up.

- How much comes in each month?

- How much goes out?

- How much goes to debt?

- How much goes to necessary expenses?

- How much goes to impulsive spending?

- How much could be saved?

- How much is being wasted?

Many times, financial disorder continues because the person does not want to look at reality. But looking at reality is the beginning of change.

Clarity may feel uncomfortable at first, but it also brings freedom.

A budget is not a prison

Some people reject the word “budget” because they think it means limitation, scarcity, or prohibition.

But a budget is not a prison. It is a tool for direction.

A budget tells you:

- What can you spend?

- What you must protect.

- What you must pay.

- What you must save.

- What you must reduce.

- What you must prioritize.

A budget does not remove freedom. On the contrary, it can help you recover freedom because it reduces chaos and increases awareness.

A person without a budget often does not control their money. Their money controls them.

Pay yourself first

One of the most important financial principles is learning to pay yourself first.

This means setting aside part of your income before spending on everything else. It can be for savings, emergencies, investment, education, or an important project.

It does not have to be a large amount at the beginning. What matters is creating the habit.

If you only save what is left over, many times nothing will be left over.

But if you set something aside first, even if it is small, you begin training your mind to build before consuming.

Savings are not just money stored. Savings are accumulated through discipline.

The importance of an emergency fund

An emergency fund is money set aside for unexpected situations.

- It is not money for cravings.

- It is not money for appearances.

- It is not money for emotional purchases.

It is protection.

An emergency fund can help when the car breaks down, when income drops, when a medical need arises, when a repair is needed, or when something unplanned happens.

It does not eliminate all problems, but it can prevent every problem from becoming debt.

Starting with a small goal can be enough: first $100, then $500, then $1,000, and then continue building according to each person’s reality.

The important thing is to begin.

Reducing expenses without destroying your life

Managing money better does not mean living miserably. It means reviewing things with wisdom.

- Some expenses are necessary.

- Some expenses are important.

- Some expenses bring healthy joy.

- But some expenses do not add value, do not build, and cannot be justified.

The question is not only:

“Can I buy this?”

The question is also:

“Does this move me closer to or farther away from the life I want to build?”

Reducing unnecessary expenses is not punishment. It is choosing better.

Stop financing emotions with money

Many people spend money not because they need something, but because they are tired, sad, anxious, bored, frustrated, or looking for relief.

- They buy to feel better.

- They go out to forget.

- They spend to escape.

- They go into debt to fill emotional emptiness.

But emotional relief bought with money often lasts only a short time, while debt or disorder may last much longer.

This does not mean a person should never enjoy something. It means learning to recognize when you are buying out of real need and when you are buying to calm an emotion.

Peace is not built through uncontrolled spending. It is built with order, purpose, and balance.

Turning money into a tool for growth

Money can disappear into immediate consumption, or it can be used to build.

- It can be used to learn a skill.

- It can be used to pay debt.

- It can be used to create an emergency fund.

- It can be used to invest in a project.

- It can be used to improve work tools.

- It can be used to protect the family.

- It can be used to serve better.

When a person changes their relationship with money, they stop seeing it only as something to spend and begin seeing it as a tool for progress.

Small steps to stop spending everything

You may not be able to change everything overnight. But you can begin with simple steps.

- Track all your expenses for 30 days.

- Cancel subscriptions you do not use.

- Set aside a small amount when income arrives.

- Avoid impulsive purchases by waiting 24 hours before buying.

- Make a list before shopping.

- Reduce debt little by little.

- Define one clear financial goal.

- Learn about personal finance every week.

- Talk with your family about priorities.

- Stop spending to impress people who do not pay your bills.

Financial change begins with awareness and continues with discipline.

Conclusion

Spending everything you earn is a silent habit that can destroy the future. It may not feel dangerous in the moment, but over time, it produces vulnerability, stress, dependency, and lack of options.

My dear reader or friend, this is not about living with fear, guilt, or condemnation. It is about waking up. It is about looking honestly at how we use what we receive. It is about learning to manage with wisdom, create margin, reduce disorder, and build little by little.

Wealth does not begin only by earning more. Many times, it begins when we stop wasting, organize what we have, and give direction to our money.

Because every dollar you manage with wisdom can become a seed.

And a seed cared for with discipline can become a future.

Disclaimer — English

This article is for educational, reflective, and informational purposes only. It should not be interpreted as financial, legal, accounting, professional, or investment advice. The purpose of this content is to encourage awareness about financial habits, money management, saving, budgeting, discipline, and personal responsibility.

Every person has a different financial reality. Income, expenses, debt, family responsibilities, emergencies, opportunities, and results may vary depending on each situation. Recommendations about saving, reducing expenses, or building an emergency fund should be adapted to each person’s ability and reality.

This content is not intended to judge, blame, or shame anyone facing financial difficulties. Lack of financial stability can be influenced by personal, family, social, employment, economic, health-related, and structural factors.

Before making important decisions related to money, debt, investments, business, family budgeting, or personal finances, it is recommended to consult a qualified professional.

Debe estar conectado para enviar un comentario.